![]()

How can the dollar collapse

in Iran?

An

explanation

by Rudo de Ruijter,

independent researcher, Netherlands

The facts below explain why and how the new

euro-denominated oil bourse (opening on March 20, 2006 in Tehran) will cause

the collapse of the US dollar.

This is a far more important issue, than the US

allegations about an Iranian nuclear threat. These allegations

may well appear to be a smoke-screen.

Take 60 seconds to understand the key of the real

issue.

1. How, since decades, does the US succeed to import

more than it exports?

2. How did Saddam spoil the game?

3. How would the dollar collapse in Tehran?

1. How, since decades, does the US succeed to

import more than it exports?

US debt is about 8,000,000,000,000 dollars. 45 percent

is due to foreigners. How can the US incur such high debts?

Thanks to OPEC's agreement (1971 and 1973) oil is

exclusively sold in US dollars. This creates a permanent demand for dollars on

the exchange market. Roughly 85 percent of the oil trade takes place

completely outside the US. The related dollar cycle goes from exchange market,

via oil purchasing countries, to oil producing countries, which spend them in

different countries, which in turn bring them back to the exchange market.

Back on the exchange market there are, generally and since decades, always

dollars missing (more demand than supply.)

Reasons:

a. The volume and price of the traded oil generally

increases. More dollars are needed over time.

b. Thanks to free trade, many dollars stay in use in international trade

outside the US.

c. Many foreign central banks keep

dollars as strategic reserves.

d. The US Treasury issues bonds, which when sold to foreigners, reduces the

amount of dollars available abroad.

So for decades, foreigners always needed more dollars. The US treasury issued

extra dollars. And here it becomes very interesting. There is only one way to

make these dollars available abroad. Spend them around the world! The US

would purchase goods, services, shares, investments etc. But the US never

had to deliver anything in return. Foreigners needed these dollars to buy oil.

The purchases were just inscribed on the trade balances and the amounts

added to the US foreign debt. For the US, the oil trade works like a fairy credit

card. Each time more dollars are needed abroad, this means "free"

shopping. Nothing can be done about it.

2. How Saddam spoiled the game

Saddam switched to the euro on November 6th, 2000. The

exchange of the Iraqi dollar reserves soon followed. It created an overflow on

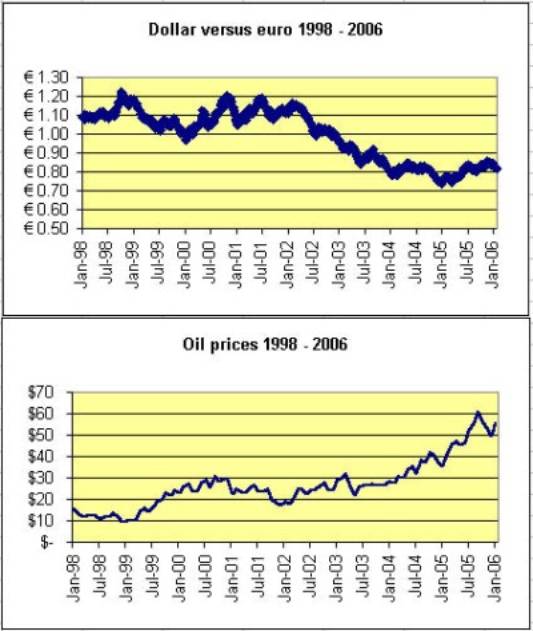

the exchange market and the dollar started its descent. (See graphic.)

Considerable numbers of international traders and investors reacted by

switching away from the dollar. Central banks would sooner or later have to

exchange a part of their dollar reserves, too. By the end of 2002 the

dollar had lost 18 percent. On March 20, 2003 the US invaded Iraq. On June

6th, 2003 the oil trade was switched back to dollars. However, the descent of

the dollar merely halted. In the meantime Iran had switched to the euro, too.

3. How can the dollar collapse in Tehran?

Iran has switched to the euro as of spring

2003. Versus the euro, and since the start of its descent, the dollar is

30 percent down now. The next Iranian step away from the dollar

is the euro-based oil bourse (foreseen starting March 20, 2006). The

sole fact that there will be another world oil price quote, independent from

IPE and NYMEX, will leave the US dollar without defence, as soon as one single

oil producing country switches away from the dollar.

If an oil producing country switches away from the

dollar, the dollars related to its oil trade become superfluous and overflow

the exchange market. Basically the US has three ways to get rid of the

overflow:

1. withdraw the dollars from the exchange market by issuing

bonds;

2. get the dollars back into the oil trade by letting

the oil prices rise on IPE and NYMEX;

3. export more than import.

Method 1 still worked partially between 2000 and 2003.

Method 2 has been used in 2004 and 2005. The oil price doubled. (This was

probably more than the Treasury had counted on. A few

hurricanes helped to push the oil prices sky high.)

If, after March 20th 2006, Teheran keeps its oil price

stable, just one switch-to-the-euro of an oil producing country will make the

dollar collapse.

The US won't be able to deal with the superfluous

dollars that will overflow the exchange market then.

Method 1 won't work: There is insuffiscient demand for

bonds. (Short term rates are already inverted.)

Method 2 won't work: Rises in oil prices on IPE and

NYMEX are more or less blocked, if Tehran's oil price remains stable.

Method 3 won't work: Increasing tremendously the US

exports, is not a feasable short term solution.

The Oil Bourse in Tehran will not only reduce the

power of IPE and NYMEX. It will also have its influence on the exchange

rate between dollars and euros. If oil gets cheaper in euros, there will

be a rush on euros. And vice versa. Many countries each have their particular

reasons to fear the upcoming bourse.

Just an extra ride in the merry-go-round of

Debts.

The strategy of a war or embargo against Iran is

shortsighted. The US may stop Iranian oil sale in euros and force the world

to buy oil in dollars again. But with a US debt rocketing at higher and higher

speed, very soon another non-dollar oil bourse (or even

several) can be established elsewhere in the world. A war or embargo would

only mean a small extra time for the dollar miracle. It would be

at a very high price.

A DETAILED OVERVIEW,

with references to sources and proofs

In 2002, most journalists did not see

what was behind the accusations that Iraq had WMDs. Today, most people do not

know what is behind the accusations that Iran has plans for nuclear weapons.

Iran's threat is not nuclear, but far more dangerous to the US. If Iran can

open its upcoming euro-based Oil Bourse in Tehran on March 20th 2006, Iran will

threaten the US dollar.

Up to 1971, each US dollar represented a fixed amount of gold. During the

Vietnam War, the US had printed and spent more money than their gold reserves

allowed. President Nixon had to abandon the gold guarantee. Since then the

dollar value is determined by the law of offer and demand on the exchange

market.

Normally, the exchange rates between currencies reflect the health of their

countries' trade balances. Countries that export more than they import will see

their currency rise in value, and countries that buy more than they sell will

see the value of their currency decrease.

This is the case for all other currencies, but not for the US dollar. For 30

years the US has imported much more than it exported, and the trend is

worsening. [1] Normally, this should make the currency fall in value, but the

dollar has not fallen. How is that possible?

The same year Nixon abandoned the gold standard, the Oil Producing and

Exporting Countries (OPEC) agreed they would only accept US dollars in payment

for their oil. This has a major advantage for the US: all other countries would

have to buy dollars first before they can obtain oil. This creates a permanent

demand for dollars.

Those foreign countries account for roughly 85 percent of the international oil

trade. [2] This is the part of the oil trade that takes place outside the US,

between oil producing countries and foreign countries.

Call it the foreign oil trade dollar cycle: dollars are bought on the exchange

market and spent in oil producing countries, which spend them in countries

around the world. Those countries offer their dollar surplus on the exchange

market and the cycle restarts.

Oil commerce always consumes more dollars. Global consumption increases, which

raises demand for the dollar and allows the US to increase its production of

dollars.[3]

Since they are needed outside the US, they have to be made available abroad.

This is where it becomes very interesting. There is only one way to get the new

notes outside the US: spend them and do free shopping around the world. (These

notes have only cost the paper and the ink.) [4]

Of course, this creates a debt, for the foreigners could use these notes some

day to buy goods, services, shares, buildings or land from the US. But since

they are now needed in the always-growing money cycle for the oil trade, there

is no need to worry about that.

This system works like a fairy credit card. Although the US has already much

too much debt, suppliers cannot refuse to deliver goods, because they need the

dollars for their oil purchases.

There are more sources of demand for dollars. Dollars disappear from the oil

trade cycle for use in international trade between countries abroad. They form

a huge amount of dollars that stays outside the US, only because of the

preference of traders to use this currency.

Nearly the whole world needs dollars, so they are accepted nearly everywhere.

Central banks, when they can, keep reserves in foreign money to protect their

own currency. To explain it simply: if ever the money market would be glutted

by their own currency, they could buy it back and offer the foreign currency in

exchange.

These foreign banks traditionaly choose to build up their stategic reserves in

the best accepted currency on the market: the US dollar.

For decades, the amount of dollars outside the US was generally growing. Each

additional dollar abroad has meant it had to leave the US, the US has spent it

abroad, and it has increased the US debt. Oceans of dollars are outside the US

today. However, when traders lose their preference for the dollar, huge waves

might overflow the exchange market and make the dollar drop.

The US Treasury, the Federal Reserve, has an efficient way to pull dollar

surpluses away from the exchange market: it offers bonds with interest. It is a

good way to control the rate of the dollar. Pull more dollars from the market

to see the rate go up, and pull fewer dollars from the market to see the rate

go down.

These loans cost interest. To pay for the interest the Fed issues new loans,

which adds to the interest to be paid. As a spiral the annual amounts have gone

up and continue to increase. The national debt is increasing explosively now,

at over eight trillion dollars ($8,000,000,000,000). [5] 45 percent is owed to

foreign creditors. You have to be very optimistic to believe that this debt

will ever be paid back.

The only difficulty for the Fed is to find enough foreigners to buy their

bonds. Traditional buyers are growing more reluctant. Often these are foreign

banks and companies, which already have invested a lot in dollars. They fear

that if the dollar collapses, their investments will be worthless too.

To keep the dollar miracle going, the buyers still continue to buy bonds. If

they are shortsighted, they will think they get interest. If they observe

better, they will notice they have to buy additional bonds first and that the

interest is paid with their own money.

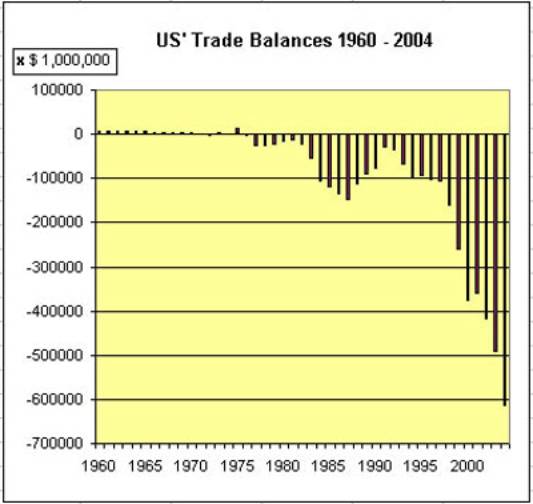

Each year the US buys more goods than it sells. For the year 2004, the shortage

on US commercial balance was six hundred and fifty billion dollars

($650,000,000,000), meaning that in average each US citizen enjoyed $3,000 more

imported products than he or she earned.

You can express it as "the average productivity is too low" or

"the government spends too much money". For instance, on the high military

cost to fulfil the neoconservative dream to rule the world. [6] It will be an

empire on credit, based on a strategy to keep the demand for dollars going, the

dollar rate high enough, and Treasury Bonds attractive.

Iraq

Of course, Iraq's destiny had already been sealed in the neo-conservatives'

plans even before Bush Jr. entered the White House. In their eyes it is natural

that the US should dominate the Middle East.

The US is world's biggest oil consumer (25 percent of global oil consumption)

and most of world's oil reserves are in the Middle East: Saudi Arabia (26

percent), Iraq (11.5 percent), Kuwait (10 percent) and Iran (13 percent).[7]

Iraq seemed already under control, as it had been paralysed since 1991 by the

embargo. The UN and US had inspected the country during many years without

finding anything suspicious. Sadam seemed already beaten.

However, he still had a trick. Since 1997, Iraq had been allowed to export oil

in the Oil For Food program. In 2000 Sadam asked the UN to convert the account

of the Oil For Food program from dollars into euros. The UN had no legal base

to refuse it [8] and from November 2000 Iraq sold its oil in euros.

As a result, the oil trade dollars became superfluous and overflowed the

money exchange market, soon followed 10 billion from Iraqis dollar

reserves. The dollar rate went down.[9] Seeing the dollar rate lowering,

many operators in the rest of the world trade switched to the euro too, which

lead to new waves of dollar offers on the exchange market and lowered the

dollar rate further.

For the US it normally does not seem a big deal to absorb surpluses of dollars

by issuing Treasury Bonds, as long as there are enough foreigners to buy them.

Once the dollars are absorbed, offer and demand would be stabilized again.

Nevertheless, Iraq's switch to the euro reduced the market share for the

permanent demand for dollars, and thus this reduced the upward force on the

dollar rate.

When the world oil price would rise again, there would not be any extra dollar

needed in the Iraqi oil trade. It would permanently limit America's free

shopping. Most painful, the US had no unlimited access to Iraqi oil anymore. It

had to buy euros to dispose of it.

In 2002 the fall of the dollar became more dramatic. The White House spread

lies about WMDs and prepared to invade Iraq. Unfortunately the international

community appeared to be reluctant. Meanwhile the dollar continued falling.

In March 2003, the US overruled the Security Council and attacked Iraq. On June

6, 2003 the Iraqi oil trade was switched back from euros to dollars. [10]

Iran

In spite of Iraq's switch back to dollars, the fall of the dollar merely

halted. [9] In the spring of 2003 Iran had started to sell their oil in euros

too. (Iran had announced its intention already in 1999, but Sadam actually

switched to the euro in November 2000).

Iran's move to the euro is logical if you realize that Iran sells 30 percent of

its oil production to Europe and the rest mainly to India and China. The

Iranian oil price was still labeled in US dollars, but customers did not have

to exchange their money into dollars anymore.

From August 2003, the euro continued its march upwards and the dollar continued

to go down. Again huge amounts of superfluous dollars from the oil trade

overflowed the exchange market and had to be mopped up by issuing Treasury

Bonds. However, this would not repair the needed permanent demand level.

It was not feasible to Invade Iran and turn the oil trade back into dollars, so

a less popular method had to be used. The oil price should rise. This pumps the

dollars into the oil trade again. For each extra dollar needed by the US, seven

times more dollars are needed abroad (as 85 percent of the international oil

trade takes place outside the US).

To make up for the loss of the Iranian trade the price increase had to be

substantial. US' military spending needed extra credit, and thus extra oil

price increases. The prayers of the treasury have been heard. Between July 2004

and September 2005, spot prices doubled. [11] A few hurricanes helped US

citizens, and the rest of the world's oil consumers, accept the new policy.

To see Iran in the euro-camp is not pleasant for the US. It creates a growing

demand for euros. On the contrary, the market share for the permanent dollar

demand becomes narrower and so does the acceptance of the dollar in

international commerce. Between July 2004 and July 2005 the part of the dollar

in world trade went down from 70 percent to 64 percenet. A little bit less than

half of those 64 percent represents America's part in world trade.[12]

Oil bourse in euros

However, the biggest change has to come next month. On March 20, 2006, the

Iranians want to start an oil bourse in Teheran, with prices in euros.[13]

This can have big effects on the exchange rate between dollars and euros. If

the oil price in euros gets lower than the oil price in dollars, there will be

a rush on euros. And if it the oil price in euros gets higher than its price in

dollars, there will be a rush on dollars.

So, basically Teheran gets an influence in the exchange rate of the currencies,

which means risks for both the US and Europe. Today Teheran is pressured and

threatened by both. Fluctuations in exchange rates might also bother China's

exports to the US.

The New York based NYMEX and London based IPE would lose a lot of their power

to set the world's oil prices. Normally, since Tehran's bourse has to be

attractive for oil producers and oil consumers, it would not be logical to

expect important differences in price with the dollar-based markets. Maybe just

a bit lower, to build up a market share.

Each loss of market share of NYMEX and IPE is a big problem for the US, since

it determines world's permanent demand for dollars. But the problem can also

become much bigger. At the moment that other oil producing countries switch to

the euro, there will be new waves of superfluous dollars on the exchange

market, which take the dollar rate down.

For the US, mopping them up by issuing bonds will then hardly be possible,

since traditional buyers and central banks will prefer to convert, as least

partly, to the euro too.

Pumping the dollars back into the oil trade with rises in oil prices worked

fine in 2004. But from March 2006 this way out can easily be blocked by stabel

prices in Teheran. If prices in euros ramain stable, prices in dollars can

hardly rise.

Prayers on the NYMEX and IPE market will be rather useless then. If the US

loses its means to get superfluous dollars from the exchange market, the fall

of the dollar would be a fact.

As by coincidence the Federal Reserve has decided that from March 23, 2006 they

will not publish the M3 money aggregate anymore. To put it simply, they will

keep secret how many dollars are held in non-American banks.[14]

When the dollar falls

There are a lot of speculations about what would happen when the dollar falls.

In my opinion it all depends on what will be left of the permanent demand for

dollars. As long as the dollar rate is not based purely on US imports and

exports, any scenario of changings will turn out to be temporary. I do not say

these changings would not hurt, but in the end the US would still have its

credit card and can continue to buy on tick.

Normally, when dollars become cheaper, American products and services become

cheaper for foreigners. Instead of buying bonds, foreigners would increase

their imports from the US. Simultaneously, foreign goods will become more

expensive for the US. But once again, the US will profit from the oil trade.

Oil producers will not accept a lower value for their barrels. If the dollar

goes down 10 percent, their prices will "logically" rise 10 percent.

(In this case the price converted to euros would remain the same.)

So this would mean that the permanent demand for dollars in the oil trade rises

with 10 percent again. At some point of the fall, the upward force on the

dollar rate will be back, the US treasury will mop up the dollar overflow and

the US can continue to buy on tick again.

Outside the US many central banks detain enormous reserves of dollars and

treasury bonds. These paper mountains would shrink in value. Many industries

detain dollar denominated capital. In most cases their value will drop.

Many banks in the world hold dollar denominated assets. They will have troubles

in meeting the obligations to their clients. These difficulties may lead to a

cascade of bankrupts.

The essence of the problem

The essence of the problem is the fact you need a special currency to buy oil.

As long as the world needs dollars to buy oil, the US makes abuse of the

situation and buys on tick from the rest of the world.

The euro contains the same risks. As long as there would be a motor for a

permanent demand for euros like, for instance, an euro denominated oil bourse

in Tehran, the eurozone could make debts and let it increase indefinitely.

To avoid such debts, the eurozone would have to export the equivalent of all

euros needed outside its borders and keep the same amount in foreign currencies

in their central bank. Why would they? The credit trick worked fine for the US

during more than 30 years!

When oil producing countries would sell oil in two or three different

currencies, this simply means that the three involved countries can do the same

trick as the US does now. In the long run it would multiply the problem by

three.

The only solution for this problem would be that oil selling countries accept

all currencies on the market. Tehran has already taken into consideration to

accept more than one currency and not just the euro. Step by step.

For the outside world the diplomatic joust is about nukes, which seems more

exciting. However, since 9/11 the whole world knows that rather inexpensive

terrorist solutions are much more effective to do harm and that even a big

arsenal of nukes does not offer any protection. We are asked to believe Iran

did not notice that and still wants such old fashioned nukes. [15]

![]()

[1] http://www.census.gov/foreign-trade/statistics/historical/gands.txt

[2] http://www.eia.doe.gov

[3] printed is a way of speaking, since today many created dollars are just

numbers on bank accounts.

[4] If you prefer, you could convert the dollars into

another currency first. That makes no difference.

[5] http://www.babylontoday.com/national_debt_clock.htm (The showed amount can vary from one internet provider to another.

Probably due to internet-proxyservers that do not update often enough.)

[6] http://newamericancentury.org/RebuildingAmericasDefenses.pdf

[7] http://www.eia.doe.gov/emeu/international/reserves.html

[8] http://www.un.org/News/briefings/docs/2000/20001031.db103100.doc.html

[9] http://fx.sauder.ubc.ca/data.html

[10] Financial Times, le 5 juin 2003

[11] http://tonto.eia.doe.gov/dnav/pet/hist/wtotworldw.htm

[12] BIS (Bank for International Settlements)

[13] http://www.iranmania.com/News/ArticleView/?NewsCode=28176&NewsKind=Business+%26+Economy

[14] http://www.federalreserve.gov/releases/h6/discm3.htm

[15] Already during the Cold War the use of nukes was

limited to frighten each other. Threats and reactions on threats were matters

between presidents with red buttons. Today the reactions on threats or use of

nukes do not simply depend on presidents and governments. They are much more

difficult to control.

NOTE ABOUT GRAPHICS:

Trade Balances 1960 - 2004 are made with data

from http://www.census.gov/foreign-trade/statistics/historical/gands.txt

Dollar rate versus euro from 1998 to 2006

are made with data from http://fx.sauder.ubc.ca/data.html

Oil prices fron 1998 to 2006 are made with data from http://tonto.eia.doe.gov/dnav/pet/hist/wtotworldw.htm

LIST OF ARTICLES:

Petrodollar Warfare: Dollars, Euros and the Upcoming Iranian Oil Bourse

by William R. Clark (Friday August 05 2005)

http://usa.mediamonitors.net/content/view/full/17450

Killing the dollar in Iran, By Toni Straka, "With the world facing a daily

bill of roughly $5.5 billion for crude oil at current price levels,"

http://www.atimes.com/atimes/Global_Economy/GH26Dj01.html

America's Foreign Owners, Thursday, September 22, 2005

http://www.thetrumpet.com/index.php?page=article&id=1712

The Proposed Iranian Oil Bourse, Krassimir Petrov, Ph. D., January 17, 2006

http://www.321gold.com/editorials/petrov/petrov011706.html

Walker's World: Iran's really big weapon, By Martin Walker, UPI Editor 1/19/2006

http://www.upi.com/InternationalIntelligence/view.php?StoryID=20060118-052333-1392r

Behind the mad rush to bomb Iran, Webster Tarpley, Jan 25 2006

http://www.pressbox.co.uk/detailed/International/BEHIND_THE_MAD_RUSH_TO_BOMB_IRAN_-_Teheran_s_Euro-Based_Oil_Exchange_Spells_Doom_for_Dollar_-_Interv_50885.html

Short articles, February 06, 2006

http://www.whatreallyhappened.com/archives/cat_iran.html

Petroeuro, From Wikipedia, the free encyclopedia

http://en.wikipedia.org/wiki/Petroeuro

Trading oil in euros - does it matter?, by Cóilín

Nunan, Published on 30 Jan 2006 by Energy Bulletin. Archived on 30 Jan 2006.

http://www.energybulletin.net/12463.html